Alpesh Shah, Managing Director & Senior Partner, Boston Consulting Group, Swayamjit Mishra, Partner, BCG, Aarav Shah, student, Bombay Scottish School

As India, with current under-penetration and scale as the most populous nation in the world, begins its journey to insure a billion adults, all the stakeholders of the insurance industry have a tall task to accomplish

It is really surprising and somewhat embarrassing that even after more than 20+ years post privatization, India is still at only 25-30% adult lives covered by life / health insurance.

Over the recent few years, as a nation, we have worked on two dimensions to try and change this situation.

Firstly, the government / regulator has defined and declared a measurable ambition of achieving “Insurance for All” by 2047.

Secondly, the government has followed through on the vision by launching various universal insurance coverage schemes. With programs like PMJJBY (Pradhan

Mantri Jeevan Jyoti Bima Yojana), PMSBY (Pradhan Mantri Swasthya Bima Yojana) and PM-JAY (Pradhan Mantri Jan Arogya Yojana), we have seen early signs of improvement in insurance penetration.

A case in point being PMJJBY which has already covered nearly 16 crore Indians. These bottom-of-the-pyramid success stories complement the strong penetration within India’s affluent segment concentrated in the metros and Tier 1&2 cities where financial literacy, insurer focus and affordability have driven penetration over the last 20+ year. As a result, there is strong momentum at the top-of-the-pyramid led by the insurers and an increasing focus at the bottom-of-the-pyramid through the government promoted schemes.

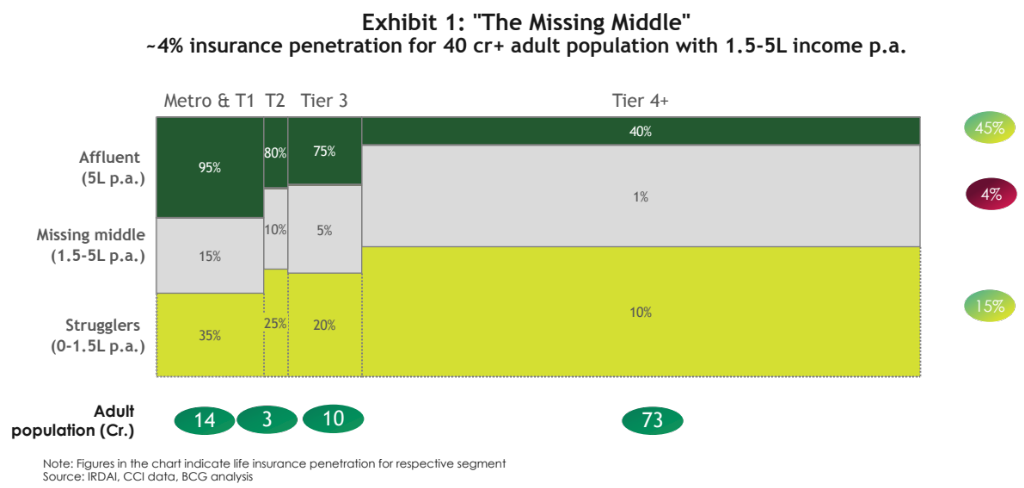

However, on dissecting the Indian insurance penetration story, there is the curious case of the missing middle, over 40% of our adult population whose insurance needs are not catered to structurally by any of the above programs or insurers.

As seen in Exhibit 1, the middle segment – households with annual income between 1.5 and 5 lakh, nearly 40% of India, have an estimated insurance penetration of less

than 5% in the case of life insurance.

The conundrum of the missing middle is best exemplified by an example about term insurance.

Today, private sector life insurers offer term insurance with minimum sum assured of INR 25 lakh and onwards while the PMJJBY scheme offers a one-year fixed term plan with sum assured of merely INR 2 Lakhs. What coverage can citizens with annual incomes in the range of INR 1.5-5 lakh secure? Applying the traditional thumb-rule of sum assured being 5x of annual income, the “missing middle” segment needs coverage in the range of INR ~7.5-25 lakh sum assured, which is not offered. This segment, hence, is excluded by most insurers and significantly under-protected if covered by PMJJBY.

How do you reckon India compares vis-a-vis other nations in life insurance penetration? Well unsurprisingly, not so well.

On a global scale, India lags developed economies significantly in terms of insurance penetration. Among the developed western nations, US and France both have nearly 90% of their adult population covered. Some emerging market peers like South Africa and Thailand also have high insurance penetration in the 70% range. Beyond penetration, we also lag behind in the level of coverage. Our life insurance protection gap is among the highest in the world, at ~83% compared to 55% for Singapore or ~41% for Hong Kong (as per SwissRe estimates).

The gap is just as stark in health insurance with only 30% of India’s population covered. Unfortunately, an average Indian today bears ~60% of total health-care costs out-of-pocket signaling a huge financial strain in the times of rising healthcare costs.

In the above context, it is imperative for India to accelerate its insurance penetration as well as address the massive under-insurance even amongst those with insurance. And the “missing middle” holds the key. We have identified five fundamental steps that India as a nation must undertake to surmount this challenge (Refer exhibit 2):

Drive an all-pervasive awareness campaign: First and foremost, as a country we need to tackle the bogey of awareness, as in the lack of it, with a high decibel all-pervasive ground level awareness campaign that drives home the fundamental value and need for insurance. This campaign could be digitally aided akin to the massive drive to successfully vaccinate 1Bn+ Indians vs. Covid-19 and that too twice in a short span of 18 months. A well thought through centrally aided campaign led by IRDAI and incentivized by the Union and State governments is the need of the hour. The insurance industry could do well to borrow a page from India’s mutual funds industry to really drive insurance awareness across both the middle-income segment and the bottom-of-the-pyramid.

An excellent example is the “Mutual Funds Sahi Hai” campaign driven by AMFI which has been the corner stone of the strides made in mutual funds’ adoption in India in recent years. Or if we dial back a couple of decades, the way India drove the “Pulse Polio awareness campaign” from house to house is something that the insurance industry could learn from.

Catch them young to drive change at population scale: Secondly, for driving lasting change at population scale, we need to embed financial literacy as a part of the school curriculum. Within one turn, read as a decade, this would fundamentally increase insurance awareness and create customer pull. Educating the next generation(s) is a very potent driver of societal change.

For example, we are sure all of us have noticed the significant move away from firecrackers that our school going children are exhibiting over the recent years. And this is primarily coming from the schools educating the young ones about the negative implications of firecrackers – from noise pollution to sound pollution to the use of child labour at Sivakasi.

There are numerous examples from Europe and especially the Nordics, where within the timeframe of a generation, the approach to driving discipline or financial planning has gotten truly embedded into citizens with early education being driven via the school system.

Create simple, fit-to-need products: A key focus area for reform the IRDAI has been driving revolves around simplifying insurance product constructs to enable rapid increase in penetration. The need of the hour is to have simple, bite sized products that are fit to customers’ needs with intuitive customer journeys.

For example, creating simple term products with 10L/15L/20L sum assured with simple and intuitive onboarding as well as seamless servicing and claims processes, could be a game changer.

Simple bundled options embedding relevant insurance in high awareness banking products could also help address the challenges around insurance being complex for our population. For example, a savings account with built-in life insurance cover where the interest earned (say on a INR 20,000 balance) is netted off with the premium due on a 5 Lakh sum assured term protection plan could be an interesting way to reach a certain segment of customers. These simplified product constructs could fundamentally change the supply context and tap into the un-insured segment in India.

Activate the affluent – “Each one gets one plus”: We believe those more fortunate have a social and moral responsibility to enable access for those in their informal employment. A campaign summarized effectively as “Each one, get one plus” would enable an increase in penetration by encouraging each affluent person/household to sponsor one or more of their dependent workers for insurance coverage.

At a relatively small sum of money for the affluent, say equivalent to a couple of cups of Starbucks a month, each of us could cover an informal worker with basic but appropriate insurance cover. With relevant social and tax-saving incentives, this could unlock a network effect stemming right from the top of the pyramid into the missing-middle or even beyond to the bottom-of-the-pyramid to drive insurance adoption. Channeled at scale, this initiative could drive penetration for 8-10 crore people by galvanizing the 40Mn+ households (expected to grow to nearly 80Mn by 2030) with income > INR 10L today.

Orchestrate ecosystems to shift from products to services – example health: The market today has very rudimentary products, for example health insurance today provides the most basic hospital cash reimbursement products. We believe that the Indian market today needs and is ready for a comprehensive end-to-end offering that could be a subscription-based service covering hospitalisation, medication, diagnostic services, out patient needs, dental needs, the works. Such a comprehensive service offering would clearly enhance the penetration manifold.

In closing, India’s journey to insuring a billion adults is well underway. We have a tall task in front of us given our current under-penetration and scale as the most populous nation in the world. But with a method to the madness that fully deploys all five of the levers identified, we could spur demand and awareness for insurance, drive a more inclusive supply of products and also, remove key friction points.

We are confident that together with these innovations and interventions, if we can activate the insurers, regulator, government and citizens, we will certainly achieve our aspiration of securing the lives and health of a billion Indians by 2030.